Select a category

Business

How the Creative Culture of Financial Literacy is Changing — for the Better

How the Creative Culture of Financial Literacy is Changing — for the Better

by Eleanor Innis

SHARE

New rules, new players and women leaders: Our economy is evolving and so is the way we learn about it.

There’s nothing like a financial crisis to ignite conversation about financial literacy. As was the case following the 2008 recession, market fears surrounding the pandemic also kickstarted a reckoning for financial literacy.

There’s been persistent financial strain on younger generations in the US — take the student debt crisis, or the battle for wage equity, or the broken promises of the gig economy, or the stratospheric cost of a first home.

Then COVID hit.. Yet many Millennials and Gen Z are they’re figuring out how to play the game in hopes of building a new system. In many ways, it’s still the same American sensibility of making dreams come true by making money, but the creative culture of financial literacy surrounding it is changing fast.

What Is Financial Literacy?

Is it developing basic money management skills, like writing a check, calculating a tip, or setting up a budget? Or is it understanding more complex topics, like investing and retirement? Does it extend to more macro topics, like understanding how a war in a foreign country impacts your country, your state, your community? The scope of financial literacy is a moving target, with new economic principles and practices influencing a constantly evolving world of money.

Image via Survey of the States

It’s a long fought issue that financial literacy isn’t taught in US schools. Actually, according to the Council for Economic Education's 2022 Survey of the States, 23 states require that high schools teach financial literacy. For residents outside of those 23 states (and no doubt within them, as well), the work of financial literacy is relegated to the home. Plenty of fintech startups have realized this, with a myriad of apps and products catering to parents who want to teach their kids responsible money management.

The idea of financial literacy is moot, however, if you don’t have resources. For many families living at or below the poverty line, as well as families just getting by in the middle class, it’s difficult to demonstrate impeccable money management if there’s a deficit of money to manage.

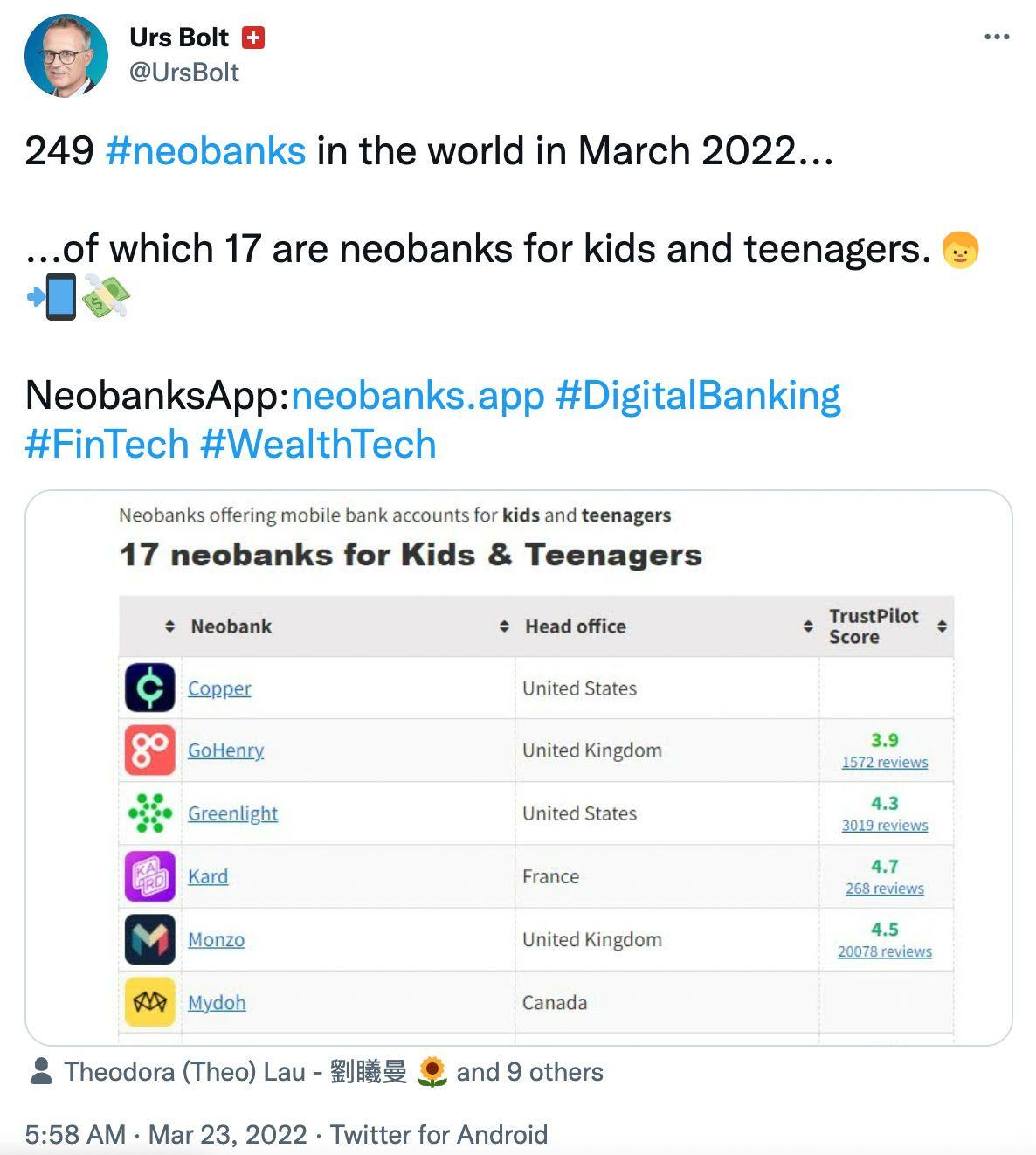

Neobanks are digital equivalents to traditional banking, and now many of them are catered to children, many with a financial literacy value prop. Image via @UrsBolt]

Kids in these socioeconomic situations are likely unable to “test drive” money by opening a money market fund or watching compound interest grow in a savings account. And when they arrive in the world as newly minted adults, they’re already saddled with student debt and mounting living expenses.

Instead, we can think about financial literacy as a baseline exposure to the right voices and to the right information. And there’s no shortage of exposure in today’s social media-dominated landscape. It’s reshaping financial culture as we know it, driven by new trends in work, new media formats, and new personalities, and it’s throwing open the doors to financial institutions and practices that have long been gatekept.

How Financial Literacy is Changing

The Way We Learn Has Changed

It’s no mystery that a majority of traditional media companies are owned by just a handful of mega-companies. This media consolidation has never truly ended — just look at how streaming services are buying up cable networks and production houses. But social media disrupts this model, offering media platforms with content made by and for the people.

It’s not a perfect system — we’ve seen how social media can spread damaging misinformation, but it has also given a platform to people, stories, and ideas that once didn’t have a chance of breaking through.

Social media has been critical in the evolution of financial literacy because the democratization of media is the democratization of knowledge. On TikTok or Instagram or Twitter you can find content centered on financial wellness and planning, delivered in a storytelling format that is truly engaging.

You can sit on your couch and discover how someone paid off their mortgage through affiliate marketing, or how someone shorted the market for a huge dividend or how someone sold an NFT in a bidding war. With the anecdotal nature of social media there comes an inherent risk, but it's unbeatable for pure discovery. Without standardized forms of gatekeeping, people are free to find tried-and-true or totally out-of-the-box ways to think about their money.

It’s the format on social media that’s especially resonant. Led by personalities and usually visual in nature, the platform totally shatters the benchmark for engagement value and staying power that a typical financial textbook could offer. For many young people, it’s a preferred channel over traditional media, from which treatments of finances and money can feel outdated and tone deaf to the struggle of younger generations.

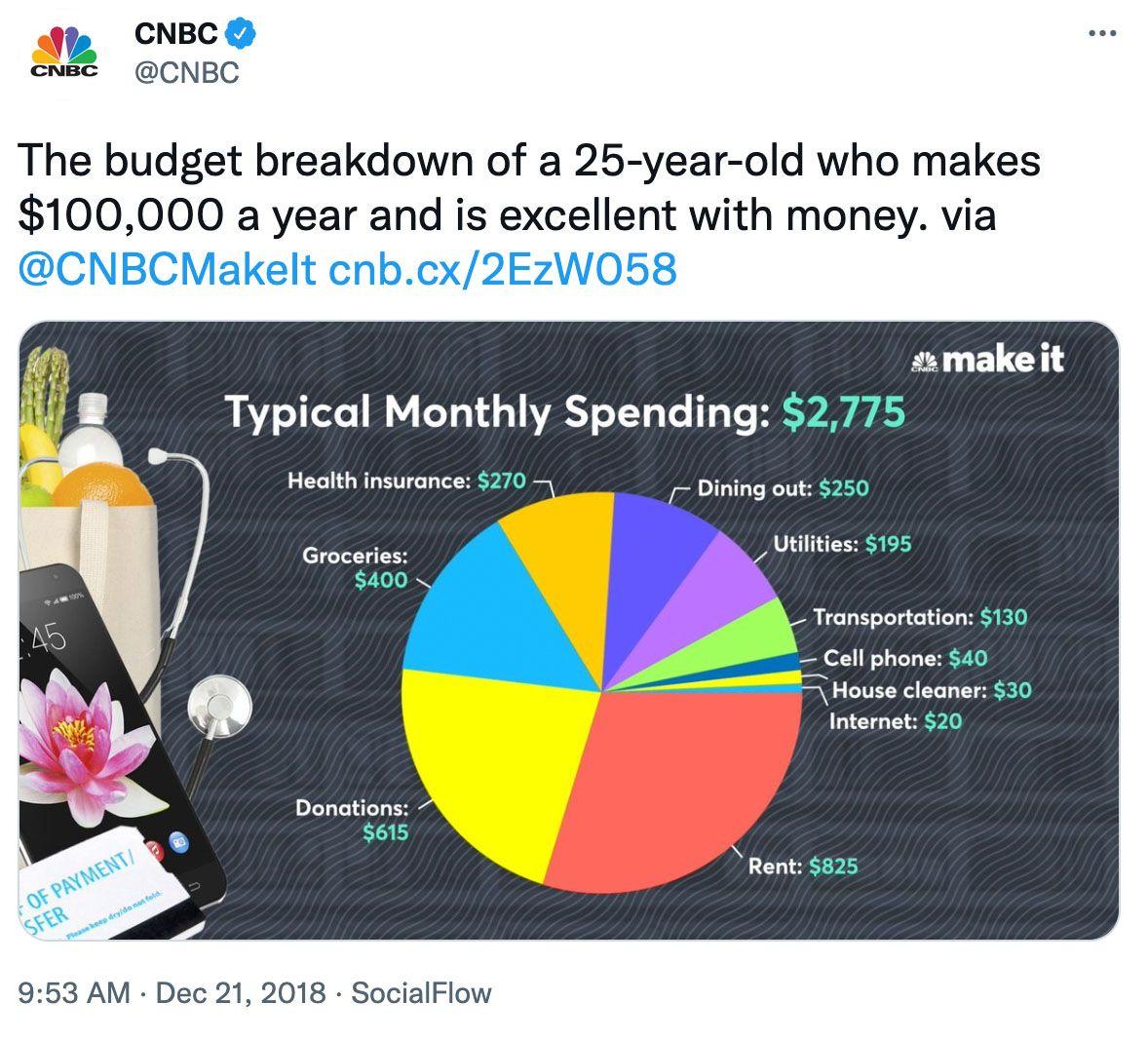

A now infamous tweet from CNBC highlighting the stunning disparities in some peoples’ financial realities. Image via CNBC]

The Way We Work Is Changing

Creator Economy. Gig Economy. Passion Economy. The Big Quit. The Anti-Work Movement. The 4-Day Work Week. You’ve probably heard these phrases frequently in the last five years. They’re all discrete phenomena, yet they represent the same thing: The way we work is changing, and it’s changing the economy in turn. These emerging approaches to work center the worker rather than the corporation, setting a precedent for more individual autonomy in work than we’ve ever seen before.

There’s a building sentiment that with traditional work, the ends don’t justify the means. In other words, many are realizing that the lifelong 9-5 grind simply isn’t worth an unfulfilling (and continually pushed back) retirement. This shift in work philosophy is necessarily a shift in money philosophy. Getting critical about work is also getting critical about how to earn. Questions arise like, Am I fairly compensated? Am I secure enough to quit my full-time job? Can a side hustle help me pay off my loan? Is there an alternative to a 401k?

This meme captures the growing sentiment of 9-5 burnout. Image via Reductress]

People are exploring new ways of working, so they need new ways of managing money. For freelancers, side-hustlers, and job-hoppers (we mean that in the positive sense), new questions rise to the surface. How much do you charge clients? What annual raise should you settle for? How do you pay taxes as an independent contractor? What about paying for health care on your own? Can you buy a home without proof of a full-time job?

Content on these topics has exploded on social media especially, galvanizing an ongoing conversation about the changing landscape of earning. Allowing for one-on-one connection and conversation, as well as instantaneous reaction, social platforms are where many young people turn to understand their options in this next generation of the workforce.

The Change Is Women-Led

In a culture built on money, women have a fundamentally different experience than other demographics. Whether it’s seeking equitable compensation in a system of wage gaps, or deciding whether to have and raise children while working, or caring for aging parents, most women must navigate a different subset of decisions that impact their earning potential and financial futures.

According to a 2022, post-pandemic survey commissioned by Wellesley College,

“sixty-one percent of young women say they are not doing well in the economy right now, with nearly one in three (29%) saying they are not doing well at all. They are facing financial anxiety, stress about finding well-paying jobs, and concern about balancing their careers and personal life in the future.”

The good news is that more and more women are sharing their stories, modeling different paths for achieving financial success. “Finfluencers” are sharing how to negotiate out of wage gaps, or how to turn out multiple passive income streams, or how to build generational wealth with non-traditional investments.

The list of finfluencers and brands creating women-centered content is growing every day — take a look at names like Berna Arnet, Tori Dunlap, Millennial in Debt.

Influencer Tori Dunlap, aka herfirst100k, is just one of many women sharing their journey to financial freedom on social media — and teaching others how to get started. Via @herfirst100k]

The uptick in content is especially resonant for Black and Latina women, who disproportionately experiece financial barriers and discrimination. In a New York Times article, Clever Girl Finance founder Bola Sokunbi lays it out on the table:

“A lot of women in our community are coming from spaces where they are the first…They’re the first to go to college and the first to earn a certain amount of money. They don’t have a lot of role models to look to.”

Like Sokunbi, some leaders are taking it further than social media, building businesses centered around financial education for women. There’s Ellevest, now a standard-bearer in investment guidance for women. The platform hinges on the idea that women invest differently than men, and deserve an investment model tailored to their unique risk level, time horizons, and goals.

Or there’s the newer Your Juno platform, made to fill the gap in financial literacy that exists for women and non-binary folks. Made by two sisters who grew up around a very money-forward mom, the app delivers financial lessons from a progressive standpoint, guiding these historically underrepresented groups how to play in a male-made system.

Thinking Ahead

Financial literacy is about so much more than balancing a checkbook. Since money converges with every area of our life, from the work we do, to what we eat, to the home we live in and the clothes on our back, it’s impossible to separate from its deep intrinsic meaning.

That’s where the culture of financial literacy is changing; it’s lending credence to money’s deep connection to ourselves. And with the growth of self-focused work and lifestyle trends, plus the expansion of social media, more people can find financial education and tools tailored to their life experience.

It’s simple — there are more ways to approach money than a state-approved curriculum can provide, and that’s why crowd-sourced financial literacy is the new norm for many.

ABOUT THE AUTHOR

Eleanor Innis

Ellie Innis is a writer, editor, and content strategist who has covered the evolving world of media and content creation for almost 10 years. She lives in Colorado where she does not ski or snowboard.